")

In my previous post, I discussed how good management can result in improved clinical treatment, better adherence to proven protocols, and ultimately lower the cost of care delivery if scaled. However, the full impact of management-based improvement is nearly impossible to realize without sufficient access to capital.

Imagine this: Dr. Ade founded a clinic nearly 20 years ago in Lagos, Nigeria. What began as a small one-room outpatient business, the clinic initially boomed because it was popular within the local community as a place to access inexpensive care. Over time, Dr. Ade bought a two-story structure from the business’ revenue, and used the site for both his clinic business and as his family home. His wife, a nurse, leads the two other nurses on staff, while he serves as the only physician, aside from external consultants when specialized services are needed.

In more recent years, Dr. Ade’s past success has slowed. Patients in his community are becoming more informed and seeking higher quality care. While he still sees a steady but dwindling stream of patients, he knows that to improve his care delivery and save his clinic, he needs to invest in improved systems. The will to improve is there, but where will he find the money?

Dr. Ade’s case is an example of just one provider within the over 50% of care provision in Sub-Saharan Africa that is delivered via the private sector[1]. Despite the size and expected future growth of the private health sector, there is minimal access to capital for healthcare businesses in low- and middle-income countries (LMICs). Data derived from studies in LMICs, including Nigeria, has shown that between 40 and 70 percent of surveyed private health care business owners intend to apply for a loan in the near future[2]. Although a strong desire for financing to expand their practices and upgrade their technologies has been seen from private health business owners, most formal financial institutions are unwilling to meet this demand.

Some of the consequences of limited access to capital are the decreased scale and scope of health care services. When credit and financing is largely unavailable, the private health sector becomes dominated primarily by small clinics, each with limited capacity. Many new physicians in credit-constrained countries rely on self-financing or loans and donations from family and friends. This leaves providers with limited funding to create clinics larger than one-man structures operating out of available rooms in their own homes[3]. Over 60% of for-profit providers are in solo or small practices consisting of outpatient facilities that support only one physician, rather than a more ideal system of consolidated three-or-more physician group practices. If more large practices are created, both providers and patients will benefit from lowered costs and increased efficiencies through economies of scale from shared resources.

Beyond an impact on scale and scope, studies have indicated that many of these small clinics do not meet the minimum quality standards set by Ministries of Health due to their limited ability to make the needed investments in assets and human capital. Essential tools to providing care, such as equipment, facilities, medical supplies, drugs, and staff, are at time financially out of reach to providers. This lack of essential resources jeopardizes quality of care and inhibits growth[4]. With access to finance having such a profound impact on the availability and delivery of healthcare, developing a proper mechanism to provide financing to private sector health MSMEs is critical to the future success of health care systems in LMICs such as Nigeria’s.

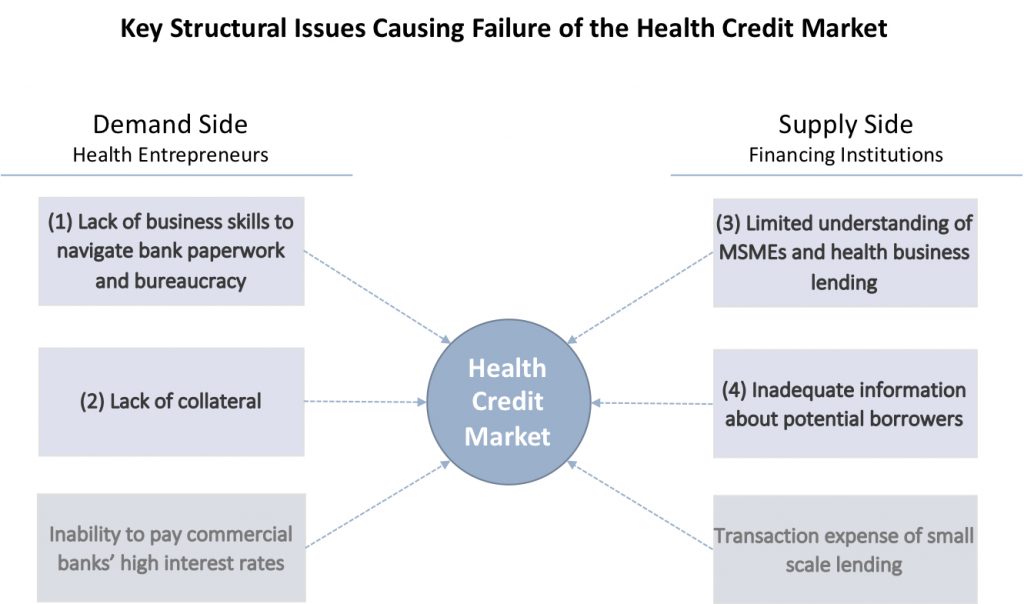

Structural Issues Hindering the Healthcare Credit Market

Business credit markets are critical to the growth of enterprises and organizations of various sizes across many industries. Despite the need, a health business credit market is largely inexistent in Nigeria due to several structural issues that ultimately hinder the growth of private health businesses. Viable health care businesses do not receive loans despite the fact that commercial banks and other lending institutions would be willing to loan the necessary funds if conditions were favorable. Under ideal conditions, lending options from financing institutions are made available on the credit market and, when entrepreneurs are in demand of financing, they seek money from the established credit market which supplies financing. When an entrepreneur and a lending institution are able to agree on the terms of a loan and the credit is disbursed, the credit market has efficiently improved the economic prospects of both parties. Alternatively, if either demand or supply side structural issues exist in the credit market and sufficiently dampen the expected financial pay-off, either the entrepreneur or the lending institution will be less willing to participate in the credit market, creating no improved economic outcomes.

Of structural issues that affect the credit market, demand-side barriers are those problems that hinder health entrepreneurs as they seek funds for their business. Health entrepreneurs includes physicians, nurses, pharmaceutical retailers, and other private sector health-related enterprises. Supply-side barriers are those issues faced by financing institutions looking to extend credit at a profit. Commercial banks, equity investors, and other holders of funding make up the supply side. The major demand-side and supply-side barriers to efficient financing within the private health sector credit market are highlighted below.

Although all these structural issues are seen in the overall SME credit market in developing countries, they are particularly pronounced in the private health credit market. Many of these issues are largely interrelated and work together to create the unfavorable situation where credit worthy health business entrepreneurs and financing institutions infrequently interact in a lending market. Only when factors align to encourage both demand and supply side parties to be present at the health credit market will sufficient levels of access to finance be seen. The four structural issue particular to healthcare will be assessed based on whether each encourages entrepreneurs and financiers to be present and participate at the health credit market, or if it discourages market presence and participation.

Demand Side

Lack of business skills to navigate bank paperwork and bureaucracy

Most MSME health care workers lack the business knowledge and financial management skills that are needed to produce basic level financial statements. Financial statements are required by banks and other providers of capital in order to assess eligibility for loans. Physicians often prefer to focus on clinical care and tend to overlook other aspects of care delivery, such as the need for tight management of staff and resources, the need to understand their business’ cash flow structure, and the importance of keeping records of daily business activities.

This limited business and financial management capacity makes the health sector appear as high-risk to investors. Financing institutions are skeptical about the profitability of lending to the health sector, especially with scanty information from health entrepreneurs about their business. Financiers are therefore less likely to participate in the private health credit market if health businesses are unable to supply financial information, a standard requirement and practice in other industries. Health entrepreneurs’ lack of business and financial skills has become a key barrier to their accessing credit, and further hampers the growth of the industry.

Lack of Collateral

The lack of collateral, or the sub-standard types of collateral that health businesses are able to provide, make the sector less attractive to financing institutions. While larger health businesses such as established hospitals and pharmaceutical manufacturers are able to provide land or buildings as collateral for loans, most small health businesses are either unable to provide adequate collateral, or only able to secure loans with equipment or personal guarantees.

Even with the ability to accept land, buildings, and equipment as collateral, financial institutions express concerns over the political risk of seizing hospitals and clinics in the case of a default. For these collateral risk reasons, financing institutions are less likely to participate in the health credit market. Banks are unwilling to give loans without the safety net of secured backing from the businesses behind it.

Supply Side

Limited understanding of MSMEs and health business lending

The hesitation of commercial banks to lend to the health sector stems, in part, from their lack of understanding of the needs of health care organizations and how to construct health loan facilities that meet the needs of both bank and customer. Banks lack knowledge on how to best address the needs of health care firms and, simultaneously, do not understand how the financial workings and revenue streams of healthcare organizations differ from that of most other sectors. For example, health organizations typically require longer loan repayment terms due to the high upfront costs they bear, the extended time it takes to build a steady customer base, and their cash flows are at times less stable than that of other sectors.

Without understanding the business of health care, its time frames for profitability, and its cash flows, banks are less likely to participate in the health credit market. The nuances of health enterprises need to be better understood by banks. Evidence suggests that when banks increase their knowledge on how health organizations work, they are more willing to lend to the sector as well as create internal systems that ease the lending process.

Inadequate Information on Potential Borrowers

Even without information that broadly examines the private health sector, financing institutions may be willing to move forward with lending to individuals or teams. Financiers often pay close attention to founders or management teams when making assessments of whether to extend funds. Individuals with strong track records in their fields and convincing approaches toward business growth/operations are favored for credit. However, banks and other financing institutions have noted that the Nigerian private health sector holds relatively few individuals or management teams that can effectively document their business plans and operational approach.

Moreover, an institutional void exists where accessing information on individuals is difficult in LMICs. Rather than utilizing databases and tools such as financial search engines to find information on business teams, financing institutions in LMICs often have to rely on network relationships and word-of-mouth to authenticate the information provided to them by entrepreneurs. Ideally, a more robust system will be developed and, in-time, a health financial database holding information about health-related businesses will be available for use by Nigerian financing institutions.

These core supply-side and demand-side issues to providing credit to the private health sector all have viable solutions. When the proper financial management skills are in place, when interest rates and collateral are addressed, and when increased information and comfort with lending to the sector exists, private health enterprises will be positioned to access capital and make the necessary improvements toward attaining world-class quality healthcare.

The Future for Dr. Ade and Similar Health Entrepreneurs

Today, if small-scale, managerially unsavvy providers like Dr. Ade want to gain access to capital, their choices are vastly limited to family, friends, and informal lending institutions. Fortunately, a number of initiatives have been created to address the access to capital issues to some extent. Most existing and attempted models have typically been structured with commercial banks at the core. In this model, commercial banks hold the funds, provide the actual loan facilities, and manage the loan portfolio. Such an arrangement allows for minimal disruption of already existing financial structures in a country or region. This model also enables optimal utilization of commercial banks’ core capabilities and benefits from the expert lending knowledge the banks already have. In this design, other aspects that will help ease the flow of capital are structured around the core bank credit lending system.

Another tool included within many health SME financing models is a financing guarantee. Under a guarantee, a government, donor organization, or other body with sufficient funds provides a set amount of money dedicated to supporting bank loans to the targeted sector. This pool of money serves as a reserve that banks are reimbursed from in the event of loan default. In this manner, banks are protected from the risks of lending to the health market, even in the face of issues such as lack of collateral, limited information on the market, and inadequate knowledge of individual business operations.

A further component often seen in most models seeking to increase access to capital is a technical assistance (TA) program. TA programs directly address the issue of entrepreneurs’ lack of business skills and banking system knowledge. TA programs often come in the form of business management and financial skills education or training where entrepreneurs are given the tools they would need to develop rudimentary financial statements and successfully fill out business loan applications.

Several programs have put these tools into real-world action. Fidelity Bank partnered with the Community Pharmacists Association of Nigeria to mitigate risks of offering working capital loans to pharmacies. USAID’s SHOPS program partnered with financial institutions and market stakeholders to develop model financing schemes. PharmAccess created the Medical Credit Fund to use both financing and technical assistance to strengthen healthcare SMEs in developing countries. These programs are good starts, but much more should be done across public, private, and partner organizations.

Any program that seeks to improve the amount of lending to health SMEs in developing counties must address the structural issues that create the health credit market failures. Simultaneously, health care entrepreneurs must develop the management skills, systems, and processes that will enable them to achieve high quality levels of care goods and services. The goal isn’t simply to give funds to the private health sector, but to add a layer of purchasing power on top of a foundation of good management. It is the combination of the two—good management plus adequate financing—that will help drive the future of the Nigerian health system in a more promising direction.

[1] IFC, “The Business of Health in Africa: Partnering with the Private Sector to Improve People’s Lives.” 2007.

[2] IFC, “Guide for Investors in Private Health Care in Emerging Markets”

[3] USAID, Deloitte Touche Tohmatsu, “Access to Financing: A Constraint to Private Health Sector Development”, November 2003.

[4] Munishi et al, 1995